Friday, December 14, 2012

Web Browser Market Share, November 2012 Update

Web Browser Market Share, November 2012 Update:

Note: As mobile devices are responsible for an increasingly greater portion of Internet browsing as a whole, we will now be including mobile statistics in addition to desktop figures.

Note: As mobile devices are responsible for an increasingly greater portion of Internet browsing as a whole, we will now be including mobile statistics in addition to desktop figures.

Operating System Market Share, November 2012 Update

Operating System Market Share, November 2012 Update:

Note: As mobile devices are responsible for an increasingly greater portion of Internet browsing as a whole, we will now be including mobile statistics in addition to desktop figures.

Note: As mobile devices are responsible for an increasingly greater portion of Internet browsing as a whole, we will now be including mobile statistics in addition to desktop figures.

Thursday, December 13, 2012

Below the Surface

Below the Surface:

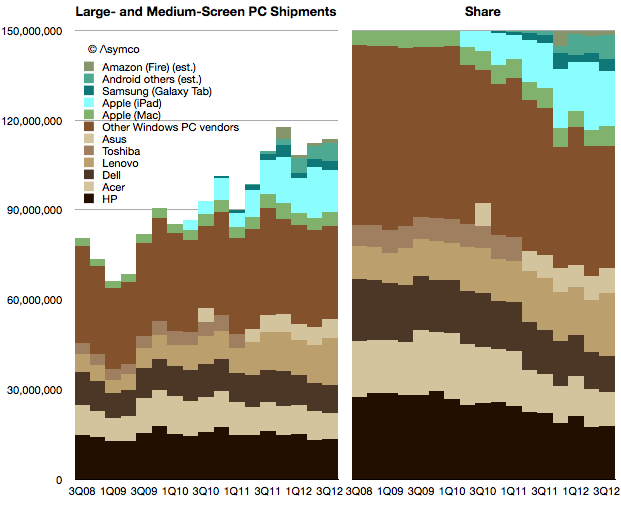

Early data shows that the PC market has not experienced a “pop” from Windows 8. Market watchers have been anticipating this pop since every previous version of Windows has led to a surge in shipments. PC vendors have also been hoping for this to lift their volumes. Volumes have been stagnant for a while, as the following chart shows:

If we combine the traditional PC and tablet markets—what I refer to as “large and medium screen PCs”— there has been growth. However the growth is all due to the tablets. When seen in a share split (blue tablets vs. brown Windows PC’s) the shift toward tablet computing is clear.

The question is whether Microsoft will be successful in shifting to this new computing model? Microsoft’s problem is not that it has difficulty offering an operating system for tablets. The problem is that the economics of both systems and application software on tablets is destructive to its margins.

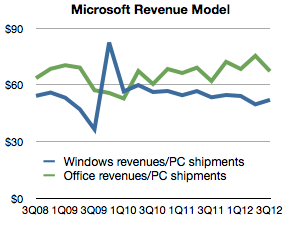

A PC has for several decades been “taxed”[1] with a Windows and Office license. The exact figure is imprecise because of subscription accounting used by Microsoft, but we can take Microsoft revenues for Windows and Office and divide by PC shipments to get an average.

This view shows how Windows revenues per PC have held steady for the last three years and Office have moved up slightly. In the latest quarter Windows “captured” $52 per PC shipment and Office “captured” $67.

The problem for Microsoft is that pricing systems software at $50 and a suite of apps at $67 for a tablet that costs $200 to the end-user is prohibitive.

Firstly because an OEM could not justify paying $50 to Microsoft while competing with another vendor whose (Android) software license costs nothing. It implies an increase in his bill of materials without the ability to charge more for the product and hence a reduction or elimination of margin.

Secondly because consumers (or IT buyers) would have a hard time justifying $67 for an Office license for every tablet when most apps are either free or under $10. (Apple charges $9.99 each for iOS versions of Pages, Numbers and Keynote which can be installed on several devices.)

The economics of tablets imply a “commoditization” of system and application software. So what’s Microsoft to do?

The answer is Surface where the software margin is captured in hardware. This explains the pricing of Surface. The price isn’t significantly below what Apple charges because Microsoft wants to capture a comparable (30%+) margin. On a $500 product that amounts to $150. After subtracting hardware operating and distribution costs we can get pretty close to the $120 it currently obtains from a PC.

This also explains the lack of appetite for “partnerships”. OEMs which would normally compete on hardware would have to deal with zero margins (or less) after license fees and would be encouraged to cut corners and shave costs, compromising the experience and causing the platform to suffer.

Microsoft does not like the phrase “post-PC” because it implies the end of its hegemony. They like to think of the PC becoming a new form factor in which they have the same role they’ve always had. However, looking beyond the form factor we see that mobility itself is disruptive in the implied modularity of the PC.

Device economics offer the explanation for an otherwise perplexing Surface strategy. The question remains how many Surface units could Microsoft possibly sell to maintain its revenues.

–

Early data shows that the PC market has not experienced a “pop” from Windows 8. Market watchers have been anticipating this pop since every previous version of Windows has led to a surge in shipments. PC vendors have also been hoping for this to lift their volumes. Volumes have been stagnant for a while, as the following chart shows:

If we combine the traditional PC and tablet markets—what I refer to as “large and medium screen PCs”— there has been growth. However the growth is all due to the tablets. When seen in a share split (blue tablets vs. brown Windows PC’s) the shift toward tablet computing is clear.

The question is whether Microsoft will be successful in shifting to this new computing model? Microsoft’s problem is not that it has difficulty offering an operating system for tablets. The problem is that the economics of both systems and application software on tablets is destructive to its margins.

A PC has for several decades been “taxed”[1] with a Windows and Office license. The exact figure is imprecise because of subscription accounting used by Microsoft, but we can take Microsoft revenues for Windows and Office and divide by PC shipments to get an average.

This view shows how Windows revenues per PC have held steady for the last three years and Office have moved up slightly. In the latest quarter Windows “captured” $52 per PC shipment and Office “captured” $67.

The problem for Microsoft is that pricing systems software at $50 and a suite of apps at $67 for a tablet that costs $200 to the end-user is prohibitive.

Firstly because an OEM could not justify paying $50 to Microsoft while competing with another vendor whose (Android) software license costs nothing. It implies an increase in his bill of materials without the ability to charge more for the product and hence a reduction or elimination of margin.

Secondly because consumers (or IT buyers) would have a hard time justifying $67 for an Office license for every tablet when most apps are either free or under $10. (Apple charges $9.99 each for iOS versions of Pages, Numbers and Keynote which can be installed on several devices.)

The economics of tablets imply a “commoditization” of system and application software. So what’s Microsoft to do?

The answer is Surface where the software margin is captured in hardware. This explains the pricing of Surface. The price isn’t significantly below what Apple charges because Microsoft wants to capture a comparable (30%+) margin. On a $500 product that amounts to $150. After subtracting hardware operating and distribution costs we can get pretty close to the $120 it currently obtains from a PC.

This also explains the lack of appetite for “partnerships”. OEMs which would normally compete on hardware would have to deal with zero margins (or less) after license fees and would be encouraged to cut corners and shave costs, compromising the experience and causing the platform to suffer.

Microsoft does not like the phrase “post-PC” because it implies the end of its hegemony. They like to think of the PC becoming a new form factor in which they have the same role they’ve always had. However, looking beyond the form factor we see that mobility itself is disruptive in the implied modularity of the PC.

Device economics offer the explanation for an otherwise perplexing Surface strategy. The question remains how many Surface units could Microsoft possibly sell to maintain its revenues.

–

- A “tax” is implied only when purchases are mandatory.

Validating the Android engagement paradox

Validating the Android engagement paradox:

Following yesterday’s IBM data, Monetate released a new study showing similar data related to retail browsing but covering a period of dates from Q3 2011 to Q3 2012.

This data also shows an acceleration of mobile shopping, from 7.7% of online in Q3 2011 to 18.8% in Q3 2012.

It also shows tablets growing to take about half of mobile traffic in a very short time frame.

The data also shows the iPad taking the vast bulk of traffic among tablets (88.9% vs. 88.3% from IBM).

The data also shows the iPhone taking 61% of phone traffic (67% from IBM) with the rest being Android.

The data shows the share of iOS being 74% in Q3 while IBM reports 77% for Black Friday.

The data also shows a very small participation from Kindle and Android tablets.

Finally, by using the install base data from ComScore, the data shows an absolute and relative decline in Android engagement. Android phones went from 0.47 of iPhone engagement to 0.4 in one year.

—

If you’d like to learn more about the Asymco method, come to Asymconf. The next Asymconf will be at the end of January near San Jose. Not only will you learn about how mobile is disrupting computing, you will also get to hobnob with the likes of Om Malik, Jean-Louis Gassée and Michael Lopp.

Following yesterday’s IBM data, Monetate released a new study showing similar data related to retail browsing but covering a period of dates from Q3 2011 to Q3 2012.

This data also shows an acceleration of mobile shopping, from 7.7% of online in Q3 2011 to 18.8% in Q3 2012.

It also shows tablets growing to take about half of mobile traffic in a very short time frame.

The data also shows the iPad taking the vast bulk of traffic among tablets (88.9% vs. 88.3% from IBM).

The data also shows the iPhone taking 61% of phone traffic (67% from IBM) with the rest being Android.

The data shows the share of iOS being 74% in Q3 while IBM reports 77% for Black Friday.

The data also shows a very small participation from Kindle and Android tablets.

Finally, by using the install base data from ComScore, the data shows an absolute and relative decline in Android engagement. Android phones went from 0.47 of iPhone engagement to 0.4 in one year.

—

If you’d like to learn more about the Asymco method, come to Asymconf. The next Asymconf will be at the end of January near San Jose. Not only will you learn about how mobile is disrupting computing, you will also get to hobnob with the likes of Om Malik, Jean-Louis Gassée and Michael Lopp.

Are We Entering a “Mobile-First” World?

Are We Entering a “Mobile-First” World?:

As we approach the new year, marketers and consumers alike are asking the question of whether or not we are entering a “mobile-first” world. For years, data companies have been predicting and measuring the massive shift from desktop to mobile, and with the recent explosion of new (affordable) smartphones and tablets, that shift is happening at a more rapid pace than ever before.

Chitika Insights was recently featured in eMarketer’s article, “Trends for 2013: Making Mobile-First a Priority.” Net Marketshare found in October that global web browsing traffic had passed 10% of all web browsing traffic, and Chitika found in June that web browsing traffic in North America passed 28% in June 2012. Check out the full story below:

As we approach the new year, marketers and consumers alike are asking the question of whether or not we are entering a “mobile-first” world. For years, data companies have been predicting and measuring the massive shift from desktop to mobile, and with the recent explosion of new (affordable) smartphones and tablets, that shift is happening at a more rapid pace than ever before.

Chitika Insights was recently featured in eMarketer’s article, “Trends for 2013: Making Mobile-First a Priority.” Net Marketshare found in October that global web browsing traffic had passed 10% of all web browsing traffic, and Chitika found in June that web browsing traffic in North America passed 28% in June 2012. Check out the full story below:

What do you think – are we moving to a “mobile-first” world?Trends for 2013: Making Mobile-First a Priority

Mobile’s share of search traffic may be as high as one-third

NOV 27, 2012- For years, marketers emphasized a build-for-the-desktop-first approach, with mobile serving as little more than a sideshow. However, rapid advances in smartphone and tablet ownership have changed that equation.Consumers in the US may spend twice as much time today with desktop media as they do with mobile, but time spent with mobile is growing at 14 times the rate of the desktop, suggesting that the two could achieve parity inside a couple of years if both maintain a consistent trajectory.

Time is not the only way to measure this shift. A growing portion of internet traffic is coming from smartphones and tablets. Net Marketshare put mobile’s share of global browsing traffic at 10.3% in October 2012. This was the first time mobile had topped 10% of all browsing for the web analytics firm, and its advance might even be greater, as the figure “actually underestimates the total amount of browsing share on mobile devices, since [Net Marketshare’s] sample does not contain data on apps, like maps.”In markets such as the US with high indices of smart device penetration, an even greater portion of internet traffic comes from smartphones and tablets. Online and mobile ad network Chitika estimated mobile’s share of web traffic in North America at 28% as of June 2012.

For key media and commerce drivers such as search, mobile accounts for a growing share of total activity. Some estimates put it at as much as one-third, and possibly even higher in some verticals such as restaurants, according to investment bank Macquarie Group.These shifts away from the desktop to smart devices explain why the mobile-first drumbeat, which rose in 2012, will only grow louder in 2013. Surveys have consistently showed the deleterious effects on consumer perception of websites that are not mobile optimized. And there is a mounting expectation among consumers that brands should even offer an app-enabled experience, certainly for the top two smartphone platforms if not also for tablets.

This is less a question of choosing between a mobile site or an app and more about prioritization. Even in an increasingly mobile-first world, websites remain focal points for brands and their customers alike.

The cost of selling Galaxies

The cost of selling Galaxies:

In the post “Google vs. Samsung” I compared the profits of Google and Samsung Electronics’ mobile (aka Telecoms) division. It showed how Samsung has grown its mobile business to such a degree that, if sustained, could conceivably influence the way Android is controlled.

However, we should not analyze Samsung’s mobile group in isolation of the entire company. Samsung relies on internal transfer of technology and capacities of production which are quite unique for device vendors today. In other words, Samsung is a relatively integrated enterprise. Understanding the whole is necessary before understanding the part.

The following graph shows the sales and operating profit for Samsung Electronics as a composite of its divisions since early 2008.

As one would expect, the mobile group (Telecom) is the source of both top and bottom line growth. The group has also been leading in terms of margins and increasing those margins steadily.

The margins averaged 11% during 2007 and 17% during the trailing four quarters. This 54% increase in margin has been matched by a 55% increase in average selling price (from $151 in 2007 to $234 in the latest quarter).

One could argue however that a 17% operating margin from a group that is now leading in volume and price is still a bit weak. At its peak Nokia enjoyed a 25% operating margin, RIM 30% and HTC 27%. Apple’s iPhone operating margin is around 45%.

I think a large part of the margin story is a relatively high level of spending on SG&A (Sales, General and Administrative) which includes advertising, sales promotion and commissions. In the case of Samsung Electronics, as sales has grown these expenses have grown in proportion. As a percent of sales SG&A have held relatively steady at around 17%.

Note that as Apple’s sales have grown its SG&A has grown less rapidly resulting in a smaller percent over time. We might see Apple’s SG&A drop to 5% during the present quarter, an all-time low.

So one of the more remarkable aspects of Samsung’s success has been their willingness to increase promotional spending. Considering that their other divisions don’t require as much “marketing expense” (semiconductors, LCD certainly, and TVs and Appliances to a lesser degree due to a smaller sales growth) we can imagine that the vast majority of this promotional spending has been in support of their mobile brands, Galaxy in particular.

In fact, we can obtain advertising spend data from annual reports.

The chart above shows comparable ad spending from a cohort of technology companies as well as Coca Cola and Samsung Electronics.

It might be surprising to note that Samsung spends considerably more than Apple and Microsoft. But it also spends more than Coca Cola, a company whose primary cost of sales is advertising.

However, advertising is not the only form of promotional spending. Samsung also pays commissions and “sales promotion“. The following chart shows the value of these sales promotions relative to the ad spending budgets above.

We don’t have data on the current year since that is released after year’s end, but it’s interesting to note that promotions cost more than ads, which themselves are substantial relative to other companies.

The company also reports “Marketing Expenses” every quarter[1]. These figures appear to be the sum of Ad spending, Sales Promotions, Public Relations and a portion of “other” expenses as a part of SG&A.

When considering all marketing expenses, Samsung Electronics’ sales efforts begin to look quite astonishing.

—

Notes:

In the post “Google vs. Samsung” I compared the profits of Google and Samsung Electronics’ mobile (aka Telecoms) division. It showed how Samsung has grown its mobile business to such a degree that, if sustained, could conceivably influence the way Android is controlled.

However, we should not analyze Samsung’s mobile group in isolation of the entire company. Samsung relies on internal transfer of technology and capacities of production which are quite unique for device vendors today. In other words, Samsung is a relatively integrated enterprise. Understanding the whole is necessary before understanding the part.

The following graph shows the sales and operating profit for Samsung Electronics as a composite of its divisions since early 2008.

As one would expect, the mobile group (Telecom) is the source of both top and bottom line growth. The group has also been leading in terms of margins and increasing those margins steadily.

The margins averaged 11% during 2007 and 17% during the trailing four quarters. This 54% increase in margin has been matched by a 55% increase in average selling price (from $151 in 2007 to $234 in the latest quarter).

One could argue however that a 17% operating margin from a group that is now leading in volume and price is still a bit weak. At its peak Nokia enjoyed a 25% operating margin, RIM 30% and HTC 27%. Apple’s iPhone operating margin is around 45%.

I think a large part of the margin story is a relatively high level of spending on SG&A (Sales, General and Administrative) which includes advertising, sales promotion and commissions. In the case of Samsung Electronics, as sales has grown these expenses have grown in proportion. As a percent of sales SG&A have held relatively steady at around 17%.

Note that as Apple’s sales have grown its SG&A has grown less rapidly resulting in a smaller percent over time. We might see Apple’s SG&A drop to 5% during the present quarter, an all-time low.

So one of the more remarkable aspects of Samsung’s success has been their willingness to increase promotional spending. Considering that their other divisions don’t require as much “marketing expense” (semiconductors, LCD certainly, and TVs and Appliances to a lesser degree due to a smaller sales growth) we can imagine that the vast majority of this promotional spending has been in support of their mobile brands, Galaxy in particular.

In fact, we can obtain advertising spend data from annual reports.

The chart above shows comparable ad spending from a cohort of technology companies as well as Coca Cola and Samsung Electronics.

It might be surprising to note that Samsung spends considerably more than Apple and Microsoft. But it also spends more than Coca Cola, a company whose primary cost of sales is advertising.

However, advertising is not the only form of promotional spending. Samsung also pays commissions and “sales promotion“. The following chart shows the value of these sales promotions relative to the ad spending budgets above.

We don’t have data on the current year since that is released after year’s end, but it’s interesting to note that promotions cost more than ads, which themselves are substantial relative to other companies.

The company also reports “Marketing Expenses” every quarter[1]. These figures appear to be the sum of Ad spending, Sales Promotions, Public Relations and a portion of “other” expenses as a part of SG&A.

When considering all marketing expenses, Samsung Electronics’ sales efforts begin to look quite astonishing.

—

Notes:

- The data used in the latter three charts are available as a Google spreadsheet here.

Samsung Electronics Segment Revenues and Operating Income in Context

Samsung Electronics Segment Revenues and Operating Income in Context:

As first introduced last week, Samsung’s revenues have grown primarily due to the expanding volumes of smartphones. In today’s post I convert the revenues and operating incomes to US Dollars and compare them to a set of companies.

First, I should note that Samsung has changed both the designation of its divisions and the way it reports revenue. Broadly speaking, Samsung Electronics has four major divisions:

I tried to reconcile these various nomenclatures with color coding in the following graph. Semiconductors are blue, Display components are red, Consumer Electronics are Yellow and Mobile are grey.

Each gridline represents $10 billion.

One more point to note about revenue recognition: Relatively recently the company has switched from reporting consolidated revenues to gross revenues. This means that current sales include inter-segment sales. So, as much as it is possible, the data above shows sales from division to division as well to external customers.

When it comes to reporting operating income, the company offers four segment values: Consumer Electronics (Appliances, TV, “Digital Media”), IT and Mobile (including mobile phones), Display Panel (formerly LCD), and Semiconductor.

I used the same color coding to show the income values in the same scale as the graph showing income:

It’s now possible to compare Samsung Electronics with Google, Microsoft and Apple in terms of divisional (as a proxy for product-line) revenue and profitability over a five year period.

At this time, a portion (majority?) of Samsung’s grey area in the operating income graph represents the vast majority of profits obtained from Android across the entire ecosystem.

As first introduced last week, Samsung’s revenues have grown primarily due to the expanding volumes of smartphones. In today’s post I convert the revenues and operating incomes to US Dollars and compare them to a set of companies.

First, I should note that Samsung has changed both the designation of its divisions and the way it reports revenue. Broadly speaking, Samsung Electronics has four major divisions:

- Semiconductors. This includes memory products as well as systems such as CPUs.

- Display products. This used to be called “LCD” but has been re-named Display Products.

- Telecom. This is mainly mobile phones but includes additional products and services for telecom operators and PCs. The division has recently been re-named IM (IT and Mobile communications).

- Consumer Electronics. This group has changed names from Digital Media and Appliances to CE. The majority of sales value comes from televisions but also includes consumer electronics and appliances.

I tried to reconcile these various nomenclatures with color coding in the following graph. Semiconductors are blue, Display components are red, Consumer Electronics are Yellow and Mobile are grey.

Each gridline represents $10 billion.

One more point to note about revenue recognition: Relatively recently the company has switched from reporting consolidated revenues to gross revenues. This means that current sales include inter-segment sales. So, as much as it is possible, the data above shows sales from division to division as well to external customers.

When it comes to reporting operating income, the company offers four segment values: Consumer Electronics (Appliances, TV, “Digital Media”), IT and Mobile (including mobile phones), Display Panel (formerly LCD), and Semiconductor.

I used the same color coding to show the income values in the same scale as the graph showing income:

It’s now possible to compare Samsung Electronics with Google, Microsoft and Apple in terms of divisional (as a proxy for product-line) revenue and profitability over a five year period.

At this time, a portion (majority?) of Samsung’s grey area in the operating income graph represents the vast majority of profits obtained from Android across the entire ecosystem.

Social Media Report 2012: Social Media Comes of Age

Social Media Report 2012: Social Media Comes of Age:

Social media and social networking are no longer in their infancy. Social media continues to grow rapidly, offering global consumers new and meaningful ways to engage with the people, events and brands that matter to them. According to Nielsen and NM Incite’s latest Social Media Report, consumers continue to spend more time on social networks than on any other category of sites—roughly 20 percent of their total time online via personal computer (PC), and 30 percent of total time online via mobile. Additionally, total time spent on social media in the U.S. across PCs and mobile devices increased 37 percent to 121 billion minutes in July 2012, compared to 88 billion in July 2011.

Social media and social networking are no longer in their infancy. Social media continues to grow rapidly, offering global consumers new and meaningful ways to engage with the people, events and brands that matter to them. According to Nielsen and NM Incite’s latest Social Media Report, consumers continue to spend more time on social networks than on any other category of sites—roughly 20 percent of their total time online via personal computer (PC), and 30 percent of total time online via mobile. Additionally, total time spent on social media in the U.S. across PCs and mobile devices increased 37 percent to 121 billion minutes in July 2012, compared to 88 billion in July 2011.

The recent proliferation of mobile devices and connectivity helped fuel the continued growth of social media. While the computer remains as the predominant device for social media access, consumers’ time spent with social media on mobile apps and the mobile web has increased 63 percent in 2012, compared to the same period last year.

Facebook remains the top social network, but new social media sites continue to emerge and catch on.

Facebook remains the top social network, but new social media sites continue to emerge and catch on.

Facebook remains the most-visited social network in the U.S. via PC (152.2 million visitors), mobile apps (78.4 million users) and mobile web (74.3 million visitors), and is multiple times the size of the next largest social site across each platform. The site is also the top U.S. web brand in terms of time spent, as some 17 percent of time spent online via personal computer is on Facebook.

The number of social media networks from which consumers can choose has exploded, and countless sites are adding social features, or integrations. While Facebook and Twitter continue to be among the most popular social networks, Pinterest emerged as a one of the breakout stars in social media for 2012, boasting the largest year-over-year increase in both unique audience and time spent of any social network across PC, mobile web and apps.

For additional insights on consumers’ cross-platform social media usage and activities, view the complete State of the Media: The Social Media Report 2012.

For additional insights on consumers’ cross-platform social media usage and activities, view the complete State of the Media: The Social Media Report 2012.

The recent proliferation of mobile devices and connectivity helped fuel the continued growth of social media. While the computer remains as the predominant device for social media access, consumers’ time spent with social media on mobile apps and the mobile web has increased 63 percent in 2012, compared to the same period last year.

Facebook remains the most-visited social network in the U.S. via PC (152.2 million visitors), mobile apps (78.4 million users) and mobile web (74.3 million visitors), and is multiple times the size of the next largest social site across each platform. The site is also the top U.S. web brand in terms of time spent, as some 17 percent of time spent online via personal computer is on Facebook.

The number of social media networks from which consumers can choose has exploded, and countless sites are adding social features, or integrations. While Facebook and Twitter continue to be among the most popular social networks, Pinterest emerged as a one of the breakout stars in social media for 2012, boasting the largest year-over-year increase in both unique audience and time spent of any social network across PC, mobile web and apps.

The Apple and Samsung Profit Recipe

The Apple and Samsung Profit Recipe:

[Apple and Samsung are sucking the oxygen out of the room. What's the recipe of their profits and why are all the other OEMs struggling? In this reiteration of April 2012’s Mobile Insider, VisionMobile analyst Stijn Schuermans gives insight into sustainability and profits in the handset market.]

The mobile handset market is in turmoil. Since Apple launched the iPhone in 2007, OEMs have been rushing to jump on the smartphone bandwagon. Five years later, few have managed to do so profitably. Even if more companies are gaining a significant market share, only two seem to be making a profit out of it: Apple – the creator of the market in the first place – and Samsung, a fast follower. Attractive profit margins are elusive for most of their competitors. Some are toppling from their former glory (Nokia, RIM), while some newcomers seem to be gaining speed (ZTE, Huawei). But will they manage to become profitable? This article is based on an issue of Mobile Insider, a monthly publication by VisionMobile. that examines under-the-radar and forward-looking trends in mobile. Each issue focuses on a specific topic distilling the insights in an easy-to-digest 5-page format. Mobile Insider is part of Telco Economics, a range of strategy research and workshops that deliver a 360° view on the new economics of the mobile industry and changing role of telcos in the era of digital ecosystems.

In our recent 100M Club infographic, we provided an extensive overview of how many units each of the main platforms and vendors in the handset market ship. The biggest players don’t necessarily make the most profits, however. The table below shows the profit margins for different vendors in the first three quarters of this year, as estimated by Arete and Asymco.

The most successful companies in the handset market anno 2012 are without a doubt Apple and Samsung.

Apple, despite having only a handful of smartphone models, captures a substantial part of the market, and experiences strong growth (58% YoY increase in units and 56% YoY increase in revenue in Q3 2012). It also has an exceptional profit margin compared to its competitors.

Samsung’s handset division accounts for more than half of its revenues and for 69% of its operating profit in Q3 2012 . Operating profit margin of the division improved to 18,8% from 13,5% a year ago. In Q1 2012, Samsung ended Nokia’s 14-year reign as largest handset maker by volume.

The success of app ecosystems is driven by network effects that create lock-in, turning them into “winner-takes-all” markets. Two dominant ecosystems emerged: iOS and Android. Any handset manufacturer that missed the Android train was left behind. Notably, Nokia failed to compete using Symbian, the dominant pre-smartphone platform, which was built for OEMs, not developers, and could not keep up in the new apps-driven ecosystem world. One other company – RIM – did have a valuable ecosystem, built on a messaging network and email synchronization. However, its value went up in smoke when the foundations upon which it was built were commoditized by OTT internet services like Gmail and WhatsApp.

As barriers to entry went down, many companies small and large could now make Android smartphones. This is immediately apparent in the market concentration, which plunged after 2008 as devices became more and more uniform, as shown in the chart below. Many companies are now getting a chance in the smartphone market: the amount of OEMs with more than 2% global market share went from 6 to 10 in two years time. However, in this commodity market, market share doesn’t guarantee profitability!

Where Samsung doesn’t own a value-adding element (e.g. the platform or the retail network), the company hedges its bets. That’s why Samsung has multiple platforms and excellent operator relationships. Samsung can then reinvest those gains in R&D (e.g. bada, handset components), marketing (the Galaxy brand) or acquisitions that strengthen the competitive advantage it already has, creating a virtuous cycle.

This, however, should not be mistaken for a “done deal” consolidation of the market. The smartphone market as we know it is less than five years old. While per-capita smartphone penetration in mature markets is approaching or has already surpassed the 50% point, there is still a lot of room for expansion in emerging markets, and therefore for new differentiated value propositions.

We can see at least two opportunities left at the table. In mature markets, a company like Amazon could enter the smartphone market with a unique business model of subsidizing (self-branded) hardware to drive a content and retailing ecosystem. This is akin to operators subsidizing hardware to drive voice and data subscriptions, only here Amazon managed to have its own branded devices, which operators never managed to make a success. We discussed this “kindelization” opportunity extensively in volume 1 and volume 2 (year 1) of Mobile Insider.

Secondly, the mobile user experience is not always tuned to emerging markets, which will be the main growth markets in the coming years. This creates opportunities for value chain differentiation, for example by tuning phones for payments (of digital goods, in shops or between people) without requiring credit cards.

Next week, we’ll discuss one promising attempt to create a new profitable handset business. Chinese OEM entrant Xiaomi is putting itself in the spotlights with impressive first year sales and innovation across hardware, services, brand and business model. Stay tuned.

To sustain profitability in the commodity smartphone market, OEMs need to create a tailored value chain. Apple has done so by innovating at each point of the value chain. Among all other OEMs, only Samsung has created a unique value chain configuration by integrating across hardware production and capturing profit at multiple links of the value chain. It’s no wonder that together Apple and Samsung capture more than 98% of the profits in the handset market.

Feel free to comment – we’d like to know what you think. And don’t forget to download the report!

- Stijn (@stijnschuermans)

[Apple and Samsung are sucking the oxygen out of the room. What's the recipe of their profits and why are all the other OEMs struggling? In this reiteration of April 2012’s Mobile Insider, VisionMobile analyst Stijn Schuermans gives insight into sustainability and profits in the handset market.]

The mobile handset market is in turmoil. Since Apple launched the iPhone in 2007, OEMs have been rushing to jump on the smartphone bandwagon. Five years later, few have managed to do so profitably. Even if more companies are gaining a significant market share, only two seem to be making a profit out of it: Apple – the creator of the market in the first place – and Samsung, a fast follower. Attractive profit margins are elusive for most of their competitors. Some are toppling from their former glory (Nokia, RIM), while some newcomers seem to be gaining speed (ZTE, Huawei). But will they manage to become profitable? This article is based on an issue of Mobile Insider, a monthly publication by VisionMobile. that examines under-the-radar and forward-looking trends in mobile. Each issue focuses on a specific topic distilling the insights in an easy-to-digest 5-page format. Mobile Insider is part of Telco Economics, a range of strategy research and workshops that deliver a 360° view on the new economics of the mobile industry and changing role of telcos in the era of digital ecosystems.

The state of the handset market

Mobile handsets are expected to be a quarter of a trillion dollar market in 2012, with 1.75 billion units sold. Four out of ten units are expected to be smartphones, which considering their higher average selling price, will account for the vast majority (more than 85%) of the handset industry revenues.In our recent 100M Club infographic, we provided an extensive overview of how many units each of the main platforms and vendors in the handset market ship. The biggest players don’t necessarily make the most profits, however. The table below shows the profit margins for different vendors in the first three quarters of this year, as estimated by Arete and Asymco.

The most successful companies in the handset market anno 2012 are without a doubt Apple and Samsung.

Apple, despite having only a handful of smartphone models, captures a substantial part of the market, and experiences strong growth (58% YoY increase in units and 56% YoY increase in revenue in Q3 2012). It also has an exceptional profit margin compared to its competitors.

Samsung’s handset division accounts for more than half of its revenues and for 69% of its operating profit in Q3 2012 . Operating profit margin of the division improved to 18,8% from 13,5% a year ago. In Q1 2012, Samsung ended Nokia’s 14-year reign as largest handset maker by volume.

Smartphones play by different rules than feature phones

When Apple launched the iPhone in 2007, the basis of competition in mobile phones changed radically. Instead of performance of the device (hardware features like battery life or colour depth, software features like address book), the success of a smartphone now depended on the ecosystem it tapped into (i.e. apps, driving much wider use cases for the device).The success of app ecosystems is driven by network effects that create lock-in, turning them into “winner-takes-all” markets. Two dominant ecosystems emerged: iOS and Android. Any handset manufacturer that missed the Android train was left behind. Notably, Nokia failed to compete using Symbian, the dominant pre-smartphone platform, which was built for OEMs, not developers, and could not keep up in the new apps-driven ecosystem world. One other company – RIM – did have a valuable ecosystem, built on a messaging network and email synchronization. However, its value went up in smoke when the foundations upon which it was built were commoditized by OTT internet services like Gmail and WhatsApp.

Mobile phone production is now a commodity

Back in the day, the proprietary devices we now call feature phones followed a traditional industrial model: supply-side economies of scale were key to keeping costs down and margins up. This led to a gradual concentration of the market, resulting in a small number of dominant players, headed by Nokia. In 2008, soon after the appearance of the modern smartphone, Google launched Android, a free to use platform to build smartphones, with the explicit intention to lower barriers to entry for handset makers, and therefore commoditize the making of smartphones. Android succeeded in its goal: time-to-market decreased, development costs went down and smartphones converged into a virtually homogeneous form factor.As barriers to entry went down, many companies small and large could now make Android smartphones. This is immediately apparent in the market concentration, which plunged after 2008 as devices became more and more uniform, as shown in the chart below. Many companies are now getting a chance in the smartphone market: the amount of OEMs with more than 2% global market share went from 6 to 10 in two years time. However, in this commodity market, market share doesn’t guarantee profitability!

Apple is the innovator

According to Harvard strategy professor Michael Porter, to gain a competitive advantage companies must create a unique value chain configuration. There is more than one recipe to achieve that. Apple has chosen to innovate across the chain: the Cupertino company owns its own platform (iOS), enhanced with content (e.g. apps, music, video) and services (e.g. iTunes, iCloud) and an outstanding product experience; it has a strong, tribal brand, while on the other hand its strong control over the supply chain makes it behave as a vertically integrated company, pushing costs down and appropriating profits across the supply chain. On the distribution side, Apple is the only major OEM to partially own the retail channel, i.e. Apple stores.Among followers, only Samsung has got a unique advantage

As competition is based on ecosystems, beyond Apple only Android-carrying OEMs are still in the game. They are in a “race to the best device”, a race which cannot be won. Coming back to Porter, the only possible basis for profitability is a unique competitive advantage, i.e. a tailored value chain that is inaccessible for competitors and delivers value for consumers. The only handset maker apart from Apple who has built such a unique value chain today is Samsung. The electronics giant not only assembles handsets, but also makes a lot of the most expensive components, notably screens and chipsets. This allows the company to capture profits across the value chain, where its competitors can only capture the value of assembly. Samsung also has an excellent time-to-market and distribution network in emerging markets, as Javed Anwer explained in the Times of India recently.Where Samsung doesn’t own a value-adding element (e.g. the platform or the retail network), the company hedges its bets. That’s why Samsung has multiple platforms and excellent operator relationships. Samsung can then reinvest those gains in R&D (e.g. bada, handset components), marketing (the Galaxy brand) or acquisitions that strengthen the competitive advantage it already has, creating a virtuous cycle.

Others left behind

Samsung’s competitors either don’t have the cash to invest in a virtuous cycle (due to streaks of losses), or they have no unique value chain configuration to invest their cash in, making the spending ineffective. Nokia used to have a feature phone cash cow and strong financial backing by Microsoft, but it has divested several key value-adding elements, notable the platform, now produced by Microsoft. ZTE and Huawei are backed by a profitable network infrastructure business. For now, this money is proving ineffective at producing a highly profitable business. Money can buy high volumes and fast growth, but without a tailored value chain this growth is likely unsustainable. HTC perhaps came closest at a competitive advantage based on the HTC Sense UI and fast time to market, but this advantage is proving to be unsustainable. In the third quarter of 2012, HTC’s net profit tumbled 79% YoY, making Q3 its least profitable quarter in six years.A duopoly emerges, or does it?

The result of Apple and Samsung’s success in creating a tailored value chain, and the failure of others to do so, is that the two companies between them capture over 98% of all available profits in the handset market (smartphones and feature phones combined). In 2011, they were the top two smartphone manufacturers in volume, with a combined market share of 39% of units shipped. In the first half of this year, their combined share had risen already well above 50%.This, however, should not be mistaken for a “done deal” consolidation of the market. The smartphone market as we know it is less than five years old. While per-capita smartphone penetration in mature markets is approaching or has already surpassed the 50% point, there is still a lot of room for expansion in emerging markets, and therefore for new differentiated value propositions.

We can see at least two opportunities left at the table. In mature markets, a company like Amazon could enter the smartphone market with a unique business model of subsidizing (self-branded) hardware to drive a content and retailing ecosystem. This is akin to operators subsidizing hardware to drive voice and data subscriptions, only here Amazon managed to have its own branded devices, which operators never managed to make a success. We discussed this “kindelization” opportunity extensively in volume 1 and volume 2 (year 1) of Mobile Insider.

Secondly, the mobile user experience is not always tuned to emerging markets, which will be the main growth markets in the coming years. This creates opportunities for value chain differentiation, for example by tuning phones for payments (of digital goods, in shops or between people) without requiring credit cards.

Next week, we’ll discuss one promising attempt to create a new profitable handset business. Chinese OEM entrant Xiaomi is putting itself in the spotlights with impressive first year sales and innovation across hardware, services, brand and business model. Stay tuned.

Conclusion

The launch of the iPhone fundamentally changed the basis of competition, eliminating players without a vibrant app ecosystem (i.e. iOS or Android). Android then commoditized the production of smartphones, reducing the importance of economies of scale that had made Nokia a leader in the past and sending market concentration in a plunge.To sustain profitability in the commodity smartphone market, OEMs need to create a tailored value chain. Apple has done so by innovating at each point of the value chain. Among all other OEMs, only Samsung has created a unique value chain configuration by integrating across hardware production and capturing profit at multiple links of the value chain. It’s no wonder that together Apple and Samsung capture more than 98% of the profits in the handset market.

Feel free to comment – we’d like to know what you think. And don’t forget to download the report!

- Stijn (@stijnschuermans)

Wednesday, December 12, 2012

November Tablet Market Share Update

November Tablet Market Share Update:

In November, much of what has defined the tablet market in the past remains the same. The iPad continues to dominate, holding over 88% of tablet Web traffic market share, maintaining their lead. In second place comes Amazon’s Kindle Fire with 4.05 impressions per 100 iPad impressions, or about 3.6% of total tablet Web traffic market share 1. November marked the introduction of the latest Nexus 7 and the new Nexus 10 tablets, helping to grow the overall Google Nexus family market share to 1.03 impressions per 100 iPad impressions, or a share of around 0.9%. The Samsung Galaxy family sits in third place behind the iPad and Kindle Fire, with 2.68 impressions per 100 iPad impressions, or around 2.4% of the overall market.

To quantify this latest study on the market as a whole, Chitika Insights examined a sample of tens of millions of tablet impressions from the Chitika Ad network. This study was drawn from a date range of November 12th to November 18th 2012, and only includes traffic from the U.S. and Canada. This week was chosen in order to eliminate any Black Friday-related traffic spikes which could skew the results.

Due to the iPad’s overwhelming presence in the tablet market, with its usage accounting for almost 90% of all tablet Web traffic seen in North America, the usage of other tablets is relayed in terms of impressions per 100 iPads. A graph depicting this study can be seen below:

")

In November, much of what has defined the tablet market in the past remains the same. The iPad continues to dominate, holding over 88% of tablet Web traffic market share, maintaining their lead. In second place comes Amazon’s Kindle Fire with 4.05 impressions per 100 iPad impressions, or about 3.6% of total tablet Web traffic market share 1. November marked the introduction of the latest Nexus 7 and the new Nexus 10 tablets, helping to grow the overall Google Nexus family market share to 1.03 impressions per 100 iPad impressions, or a share of around 0.9%. The Samsung Galaxy family sits in third place behind the iPad and Kindle Fire, with 2.68 impressions per 100 iPad impressions, or around 2.4% of the overall market.

To quantify this latest study on the market as a whole, Chitika Insights examined a sample of tens of millions of tablet impressions from the Chitika Ad network. This study was drawn from a date range of November 12th to November 18th 2012, and only includes traffic from the U.S. and Canada. This week was chosen in order to eliminate any Black Friday-related traffic spikes which could skew the results.

Due to the iPad’s overwhelming presence in the tablet market, with its usage accounting for almost 90% of all tablet Web traffic seen in North America, the usage of other tablets is relayed in terms of impressions per 100 iPads. A graph depicting this study can be seen below:

The latest report yet again underscores the iPad’s dominance in the space, but also the credible competition coming from users of Amazon, Samsung and Google tablets. The 2012 holiday season will likely lead to an increased presence of Android tablets when it comes to Web browsing, but high sales predictions for the recently debuted new iPad and iPad Mini are likely to stamp out any significant share gains by Apple’s competitors. Based on long-term trends, the U.S. and Canada are at least several months away from iPad users generating anything less than 75% of tablet Web traffic.

1 Looking back at the October tablet report you will see a growth in Kindle Fire’s share of tablet Web traffic. On November 8, Amazon published a blog post detailing an extensive list of possible variations in user agent strings to identify Kindle devices. This type of transparency allows Chitika Insights, and other market researchers, to provide the most accurate data possible when reporting on the state of the Web usage market. As such, the numbers we are reporting this month for Kindle Fire have changed.

Samsung’s Capital Structure

Samsung’s Capital Structure:

Having described the Revenue, Operating Margin and cost structure for Samsung Electronics it’s time to review their investment strategy.

The Economist summarized it well:

To answer, I reviewed Samsung Electronics CapEx as reported in their quarterly cash flow statements. The following graph illustrates the data:

Note that during 2006 and 2007 the company specified expenditures on an operating divisional level. Since 2008 it has reported only a total. For the years where divisional detail is available, the percent split looks as follows.

If we combine the Semiconductor division (Memory and System LSI) with the LCD group and classify this as “components” the split looks as follows:

Therefore, for the two years when information was available, the component divisions consumed 91% of expenditures and Consumer Electronics (Digital Media) together with the Telecom (mobile phones, mainly) were a combined 9%. The least capital intensive division was Telecom, the mobile phone group, with only a 2% allocation of capital.

The other observation is that, after a contraction in the recession years of 2008 and 2009, CapEx expanded greatly in 2010 and 2011. [1]

Coincident with the growth in CapEx, the company’s revenues grew dramatically as well. However, as the graphs below show, the growth has come predominantly from the Telecom division.[2]

I calculated the correlations between each division’s revenues and the growth in CapEx (total) for the time periods 2006 to present and 2008 to present and obtained the same results: The division with closest correlation to CapEx remains the Semiconductor group.

This stands to reason. Capital expenditures are mainly in the service of semiconductor manufacturing. Semiconductors, or components in general, require more capital than assembly of devices or consumer electronics.

However, the revenues and operating income for devices have grown far faster. Samsung’s investment in capacity would have been largely profit-free had they not also been assembling the devices which capture the margins.

One might conclude that Samsung would be better off abandoning its capital-intensive components business and focusing on the devices. However, as James Allworth points out if you only do the devices, you may find yourself vulnerable to value chain disruption. Whoever is involved “upstream” in the value chain will inevitably learn the device business from a base of “commodity” manufacturing and pose a threat.

Now the question poses itself: Which of the usual suspects understands this?

Stay tuned for evidence of an incumbent response.

If you want to learn more about the future of the technology industries and the evolution of value chains, consider participating in Asymconf.

—

Notes:

Having described the Revenue, Operating Margin and cost structure for Samsung Electronics it’s time to review their investment strategy.

The Economist summarized it well:

[Samsung's] businesses look remarkably disparate, but they share a need for big capital investments and the capacity to scale manufacture up very quickly, talents the company has exploited methodically in the past.Can we find evidence of this capital intensity?

Samsung’s successes come from spotting areas that are small but growing fast. Ideally the area should also be capital-intensive, making it harder for rivals to keep up. Samsung tiptoes into the technology to get familiar with it, then waits for its moment. It was when liquid-crystal displays grew to 40 inches in 2001 that Samsung took the dive and turned them into televisions. In flash memory, Samsung piled in when new technology made it possible to put a whole gigabyte on a chip.

When it pounces, the company floods the sector with cash. Moving into very high volume production as fast as possible not only gives it a price advantage over established firms, but also makes it a key customer for equipment makers. Those relationships help it stay on the leading edge from then on.

The strategy is shrewd. By buying technology rather than building it, Samsung assumes execution risk not innovation risk. It wins as a “fast follower”, slipstreaming in the wake of pioneers at a much larger scale of production. The heavy investment has in the past played to its ability to tap cheap financing from a banking sector that is friendly to big companies, thanks to implicit government guarantees much complained about by rivals elsewhere.

To answer, I reviewed Samsung Electronics CapEx as reported in their quarterly cash flow statements. The following graph illustrates the data:

Note that during 2006 and 2007 the company specified expenditures on an operating divisional level. Since 2008 it has reported only a total. For the years where divisional detail is available, the percent split looks as follows.

If we combine the Semiconductor division (Memory and System LSI) with the LCD group and classify this as “components” the split looks as follows:

Therefore, for the two years when information was available, the component divisions consumed 91% of expenditures and Consumer Electronics (Digital Media) together with the Telecom (mobile phones, mainly) were a combined 9%. The least capital intensive division was Telecom, the mobile phone group, with only a 2% allocation of capital.

The other observation is that, after a contraction in the recession years of 2008 and 2009, CapEx expanded greatly in 2010 and 2011. [1]

Coincident with the growth in CapEx, the company’s revenues grew dramatically as well. However, as the graphs below show, the growth has come predominantly from the Telecom division.[2]

I calculated the correlations between each division’s revenues and the growth in CapEx (total) for the time periods 2006 to present and 2008 to present and obtained the same results: The division with closest correlation to CapEx remains the Semiconductor group.

This stands to reason. Capital expenditures are mainly in the service of semiconductor manufacturing. Semiconductors, or components in general, require more capital than assembly of devices or consumer electronics.

However, the revenues and operating income for devices have grown far faster. Samsung’s investment in capacity would have been largely profit-free had they not also been assembling the devices which capture the margins.

One might conclude that Samsung would be better off abandoning its capital-intensive components business and focusing on the devices. However, as James Allworth points out if you only do the devices, you may find yourself vulnerable to value chain disruption. Whoever is involved “upstream” in the value chain will inevitably learn the device business from a base of “commodity” manufacturing and pose a threat.

Now the question poses itself: Which of the usual suspects understands this?

Stay tuned for evidence of an incumbent response.

If you want to learn more about the future of the technology industries and the evolution of value chains, consider participating in Asymconf.

—

Notes:

- Some of this growth is due to a new (K-IFRS) accounting standard in use after 2010, but the expansion was significant regardless.

- The revenues data is was reported using three different accounting methods and each is shown with a different line color: Blue is “Parent basis”, Green is “Consolidated basis” and Yellow is “K-IFRS”.

Monday, December 03, 2012

Android crushes the competition in China as it passes 90% smartphone market share: Report

Android crushes the competition in China as it passes 90% smartphone market share: Report:

Android has established a clear monopoly in China after achieving more than 90 percent market share there, up from 58.2 percent a year ago, according to a new report from Analysys International (via Tech in Asia). The data combines estimates from both devices sales and ownership.

Google’s mobile OS soared to 83 percent last quarter, and it has continued its run, capturing an estimated 90.1 percent of the market. It’s possible Android’s overall share is even higher than estimated, as the firm doesn’t count knock-off phones, many of which are powered by the platform.

iOS also dropped from 6 percent to 4.2 percent. However, it may be underrepresented, as Analysys notes that it doesn’t include grey market imports. Since the iPhone 5 is not yet officially available in China, many sellers have resorted to having the device smuggled in from Hong Kong.

Nokia’s Symbian continued its tragic decline, dropping from 6 percent in the second quarter to 2.4 percent in the third. Just a few years ago, Nokia had the dominant position in the Chinese mobile market. With Nokia’s transition to Windows Phone, Symbian is on its way out, but sales of its Lumia devices are still getting off the ground.

Smartphones based on the Windows Mobile, BlackBerry and Linux operating systems took up a negligible share of the market.

Budget smartphones continued to gain momentum, as the average price for Android devices fell yet again, this time to ($223) RMB 1,393 down from $251(RMB 1,560). The average price for a Symbian smartphone came in at $179 (RMB 1,114) and iOS dropped slightly to $726 (RMB 4,523).

With Android taking over almost the whole market in China, at least according to Analysys’ estimates, the country is becoming a stronghold for the platform. Google. however, is unable to properly capitalize on its growing user base there, as many of its services are blocked or constricted.

Local Internet companies have moved in to take advantage of the opportunity. Baidu, for instance, has built its own software that works on top of Android, while Alibaba is pursuing its own mobile operating system that may or may not be based on Android, depending on who you talk to. Chinese smartphone maker Xiaomi has also thrown its lot in with Android for its MIUI ROM and Mi-One and Mi-Two smartphones.

Estimates from Analysys are worth noting because of their consistency, its interpretation of the Chinese smartphone market is just one of many. Recent third-quarter data from app analytics firm Umeng put Apple’s smartphone distribution on its platform at 33 percent.

Image via Flickr / fromkeith

Android has established a clear monopoly in China after achieving more than 90 percent market share there, up from 58.2 percent a year ago, according to a new report from Analysys International (via Tech in Asia). The data combines estimates from both devices sales and ownership.

Google’s mobile OS soared to 83 percent last quarter, and it has continued its run, capturing an estimated 90.1 percent of the market. It’s possible Android’s overall share is even higher than estimated, as the firm doesn’t count knock-off phones, many of which are powered by the platform.

iOS also dropped from 6 percent to 4.2 percent. However, it may be underrepresented, as Analysys notes that it doesn’t include grey market imports. Since the iPhone 5 is not yet officially available in China, many sellers have resorted to having the device smuggled in from Hong Kong.

Nokia’s Symbian continued its tragic decline, dropping from 6 percent in the second quarter to 2.4 percent in the third. Just a few years ago, Nokia had the dominant position in the Chinese mobile market. With Nokia’s transition to Windows Phone, Symbian is on its way out, but sales of its Lumia devices are still getting off the ground.

Smartphones based on the Windows Mobile, BlackBerry and Linux operating systems took up a negligible share of the market.

Budget smartphones continued to gain momentum, as the average price for Android devices fell yet again, this time to ($223) RMB 1,393 down from $251(RMB 1,560). The average price for a Symbian smartphone came in at $179 (RMB 1,114) and iOS dropped slightly to $726 (RMB 4,523).

With Android taking over almost the whole market in China, at least according to Analysys’ estimates, the country is becoming a stronghold for the platform. Google. however, is unable to properly capitalize on its growing user base there, as many of its services are blocked or constricted.

Local Internet companies have moved in to take advantage of the opportunity. Baidu, for instance, has built its own software that works on top of Android, while Alibaba is pursuing its own mobile operating system that may or may not be based on Android, depending on who you talk to. Chinese smartphone maker Xiaomi has also thrown its lot in with Android for its MIUI ROM and Mi-One and Mi-Two smartphones.

Estimates from Analysys are worth noting because of their consistency, its interpretation of the Chinese smartphone market is just one of many. Recent third-quarter data from app analytics firm Umeng put Apple’s smartphone distribution on its platform at 33 percent.

Image via Flickr / fromkeith

Subscribe to:

Posts (Atom)